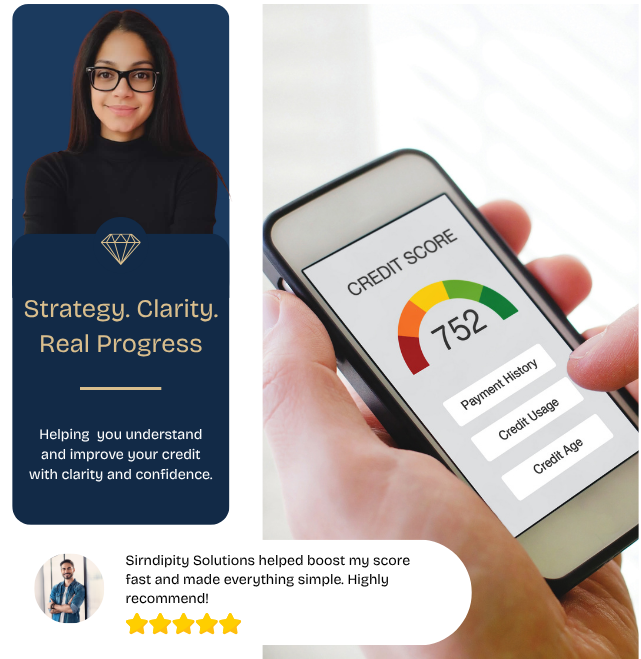

Strategically

Rebuild Your Credit

We don’t just dispute negative items— we analyze,

challenge, and rebuild your credit with a clear plan

so you can move forward with confidence.

Strategically

Rebuild Your Credit

We don’t just dispute negative items— we analyze, challenge, and rebuild your credit with a clear plan so you can move forward with confidence.

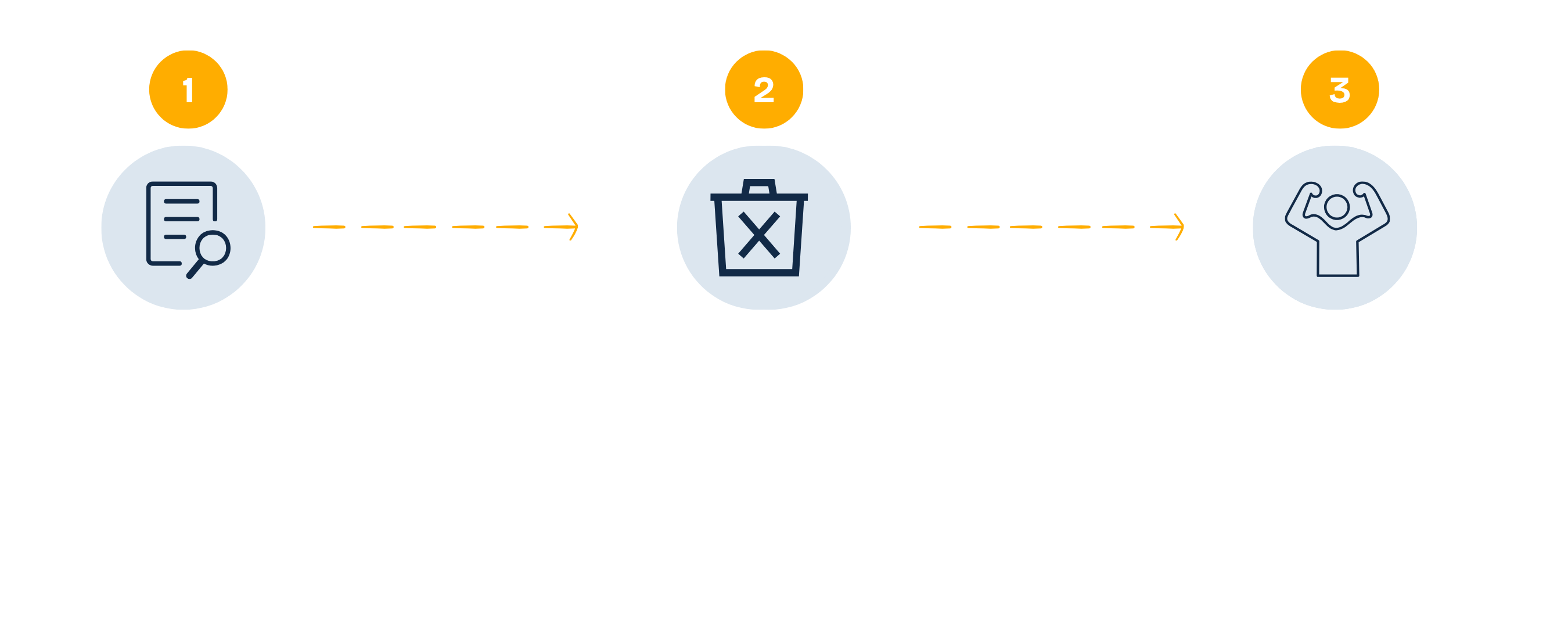

- How It Works?

A Smarter, Simpler Way to Fix Your Credit

- How It Works?

A Smarter, Simpler Way to Fix Your Credit

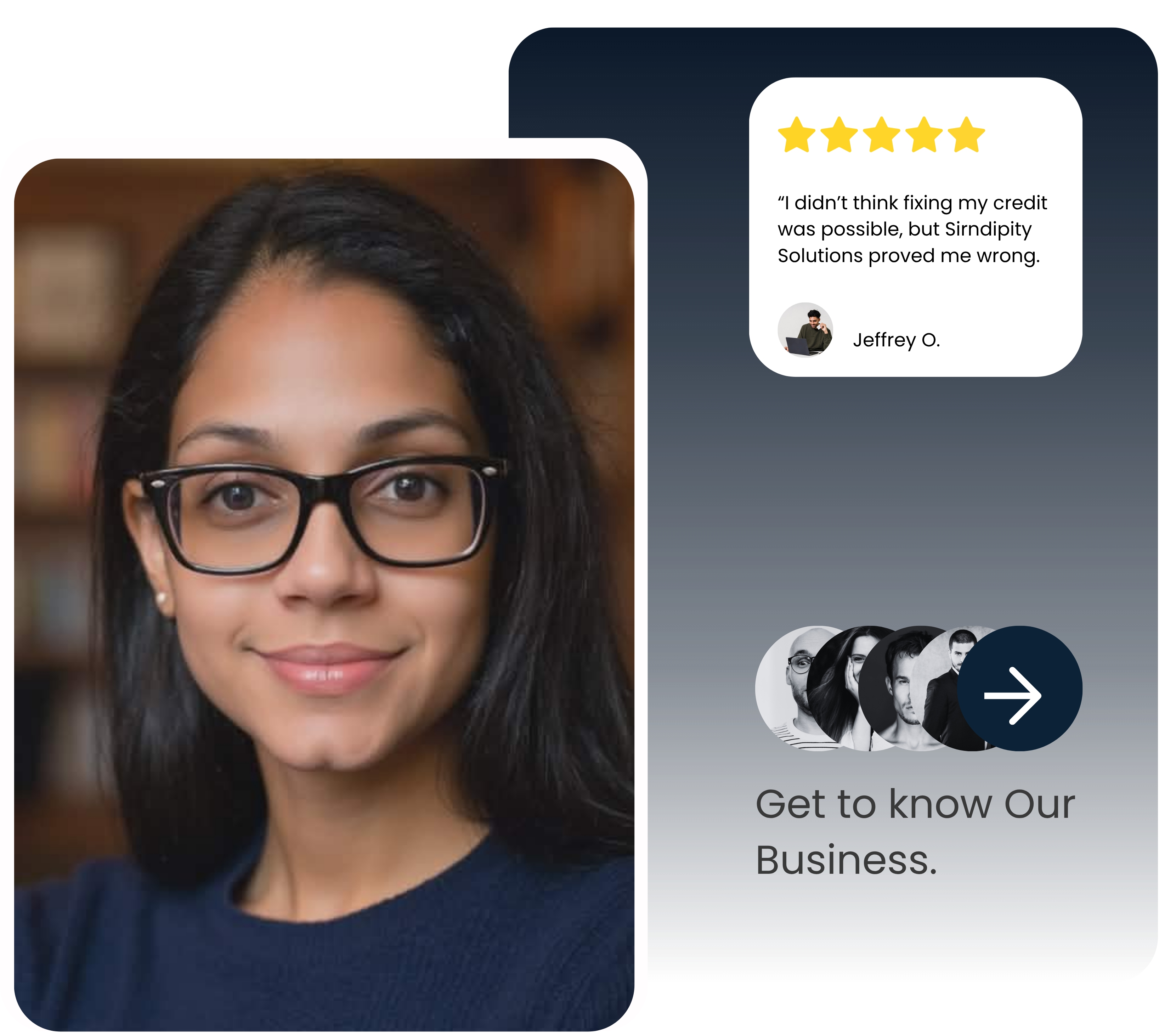

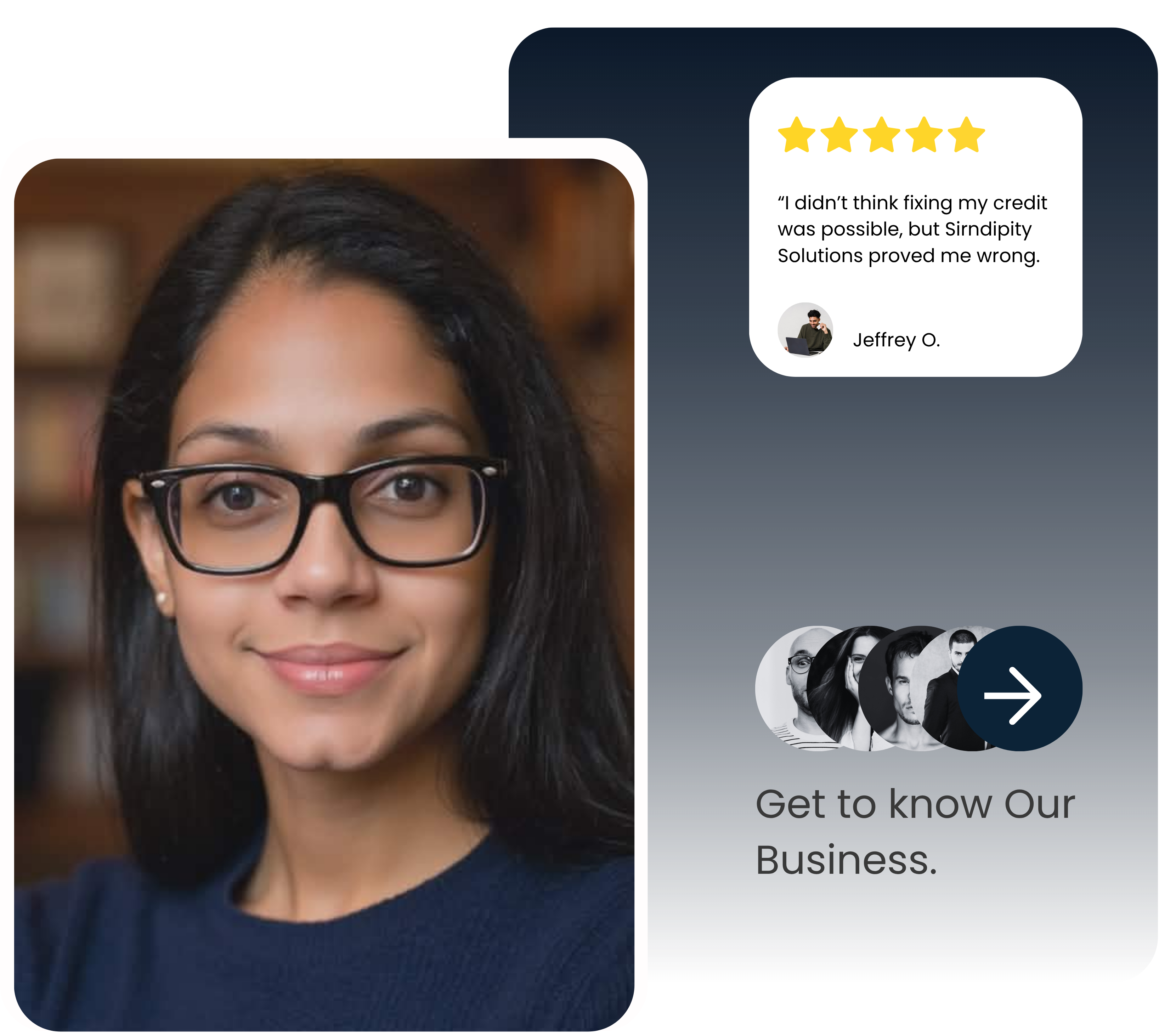

- About Us

Why I Built SirnDipity Solutions LLC

I’m a wife, a mother of three, and a full-time working professional who is very involved in my children’s lives and school activities. Like many families, my husband and I have always worked hard to build a stable and comfortable life for our children.

A few years ago, we purchased a two-bedroom condo with the intention of making it our home. Like many first-time homeowners, we were excited and committed to turning it into something special. In the process of renovating and improving the space, we relied heavily on credit to help bring our vision to life.

At the time, it felt like we were doing what we needed to do for our family. But over time, we realized we had taken on more than we could comfortably manage. As our family grew and we welcomed our second child, it became clear that our two-bedroom home was no longer enough. We began the search for a larger space where our family could continue to grow. Eventually, we found a single-family ranch-style home that felt like the right next step.

We worked with our realtor, submitted an offer, and were excited when it was accepted. But during the underwriting process, we were faced with a difficult reality—our debt from the condo renovations had significantly impacted our financial profile. In order to move forward with the new home, we needed to reduce our debt and stabilize our credit situation. That moment was overwhelming.

We found ourselves scrambling, trying to pay down balances and make quick financial decisions just to keep our dream of a new home alive. It was stressful, emotional, and eye-opening all at once. It forced us to take a step back and truly understand how credit, debt, and financial decisions impact long-term goals—not just short-term plans.

- About Us

Story Behind SirnDipity Solutions LLC

I’m a wife, a mother of three, and a full-time working professional who is very involved in my children’s lives and school activities. Like many families, my husband and I have always worked hard to build a stable and comfortable life for our children.

A few years ago, we purchased a two-bedroom condo with the intention of making it our home. Like many first-time homeowners, we were excited and committed to turning it into something special. In the process of renovating and improving the space, we relied heavily on credit to help bring our vision to life.

At the time, it felt like we were doing what we needed to do for our family. But over time, we realized we had taken on more than we could comfortably manage. As our family grew and we welcomed our second child, it became clear that our two-bedroom home was no longer enough. We began the search for a larger space where our family could continue to grow. Eventually, we found a single-family ranch-style home that felt like the right next step.

We worked with our realtor, submitted an offer, and were excited when it was accepted. But during the underwriting process, we were faced with a difficult reality—our debt from the condo renovations had significantly impacted our financial profile. In order to move forward with the new home, we needed to reduce our debt and stabilize our credit situation. That moment was overwhelming.

We found ourselves scrambling, trying to pay down balances and make quick financial decisions just to keep our dream of a new home alive. It was stressful, emotional, and eye-opening all at once. It forced us to take a step back and truly understand how credit, debt, and financial decisions impact long-term goals—not just short-term plans.

What We Help You Do

A proven process designed to get real results—without confusion or shortcuts.

Credit Report Analysis

Understand what’s impacting your

score and what to fix first.

Strategic Dispute Services

Challenge inaccurate, outdated, and unfair items.

Credit Rebuilding Guidance

Build strong credit habits for long-term success.

This Isn’t Just Credit

Repair—It’s a Strategy

Most companies focus only on removing negative items. At SirnDipity Solutions LLC, we go further. We combine credit education, strategic planning, and hands-on guidance to help you not only improve your score—but understand how to maintain it.

Because real progress doesn’t come from quick fixes. It comes from having the right strategy—and knowing how to use it.

This Isn’t Just Credit

Repair—It’s a Strategy

Most companies focus only on removing negative items. At SirnDipity Solutions LLC, we go further. We combine credit education, strategic planning, and hands-on guidance to help you not only improve your score—but understand how to maintain it.

Because real progress doesn’t come from quick fixes. It comes from having the right strategy—and knowing how to use it.

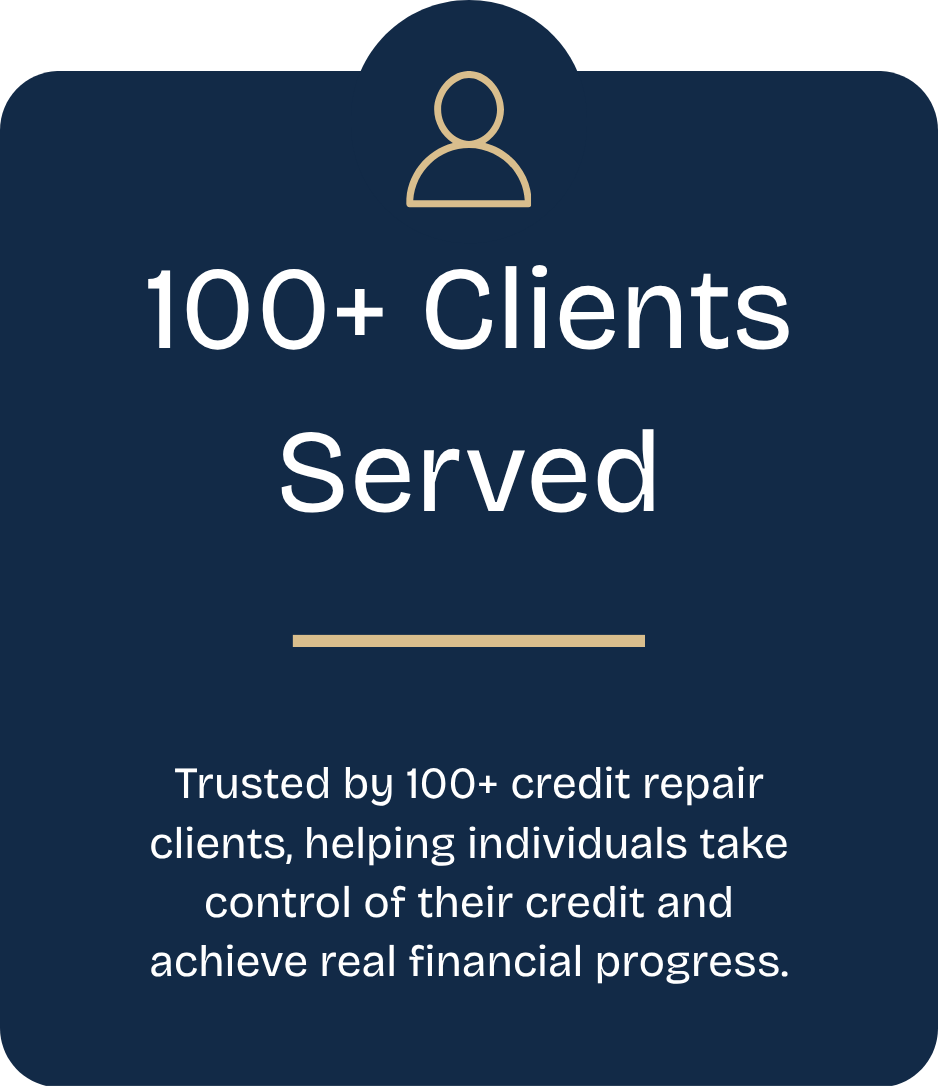

Helping Clients

Move Forward with Confidence

We help clients take control of their credit journey with clear guidance, practical solutions, and personalized support. From reviewing credit reports to identifying negative items and creating a step-by-step improvement plan, our goal is to make the process easier to understand and less overwhelming.

Helping Clients

Move Forward with Confidence

We help clients take control of their credit journey with clear guidance, practical solutions, and personalized support. From reviewing credit reports to identifying negative items and creating a step-by-step improvement plan, our goal is to make the process easier to understand and less overwhelming.

We believe in clarity—no hidden fees, no unrealistic promises.

Just a structured plan to help you move forward.

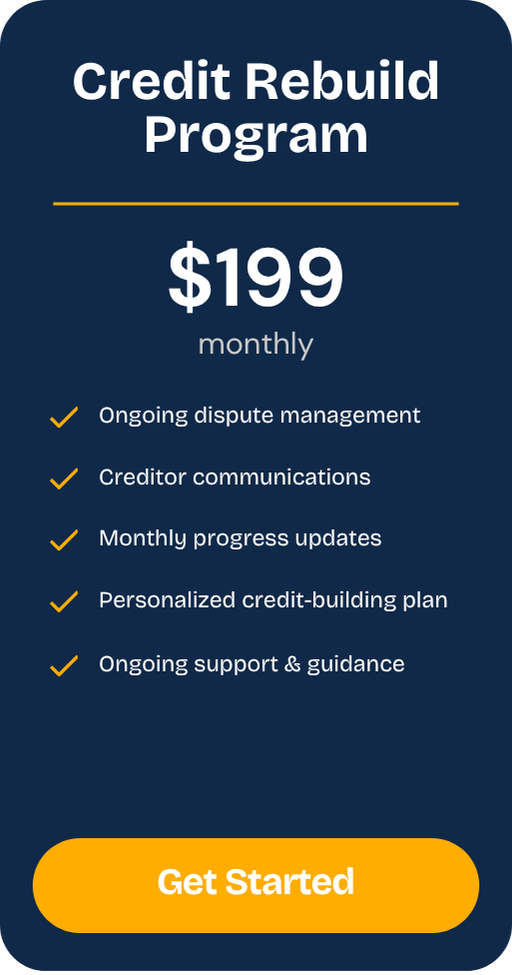

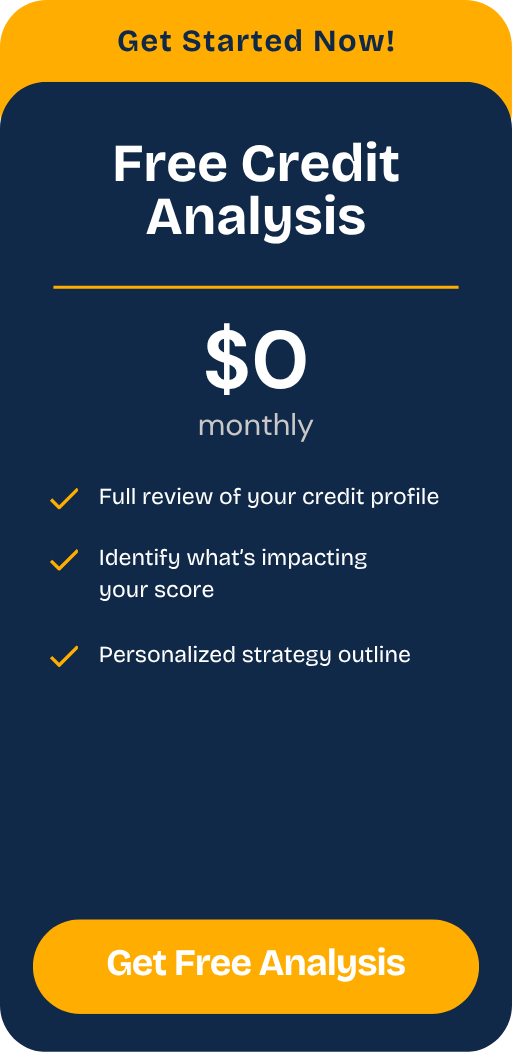

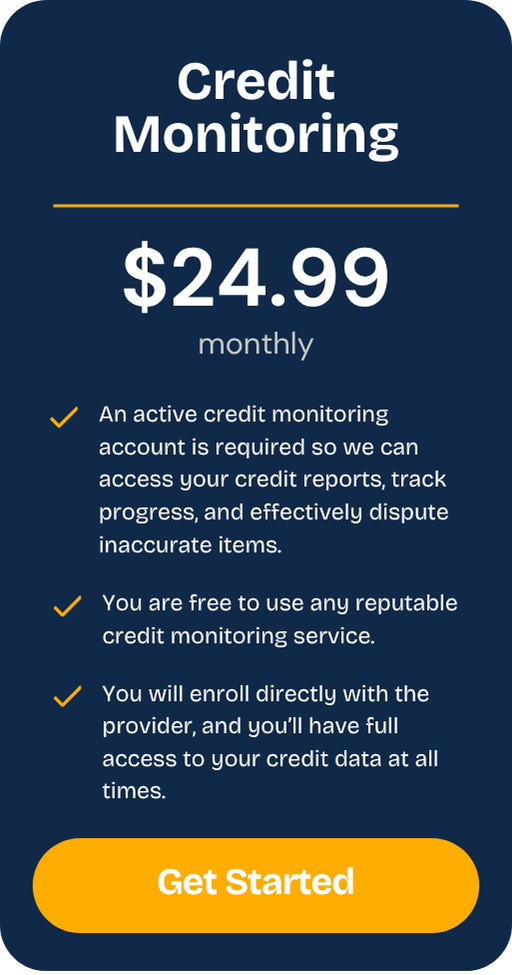

Credit Monitoring

(Required for Service)

Estimated $24.99/month (third-party provider) An active credit monitoring account is required so we can access your credit reports, track progress, and effectively dispute inaccurate items. You are free to use any reputable credit monitoring service. However, we recommend Credit Hero Score because it provides the detailed reporting and updates needed to support our process. You will enroll directly with the provider, and you’ll have full access to your credit data at all times.

Credit Monitoring

(Required for Service)

Estimated $24.99/month (third-party provider) An active credit monitoring account is required so we can access your credit reports, track progress, and effectively dispute inaccurate items. You are free to use any reputable credit monitoring service. However, we recommend Credit Hero Score because it provides the detailed reporting and updates needed to support our process. You will enroll directly with the provider, and you’ll have full access to your credit data at all times.

Your Credit Impacts More Than You Think

Your credit affects approvals, interest rates, and opportunities. When it’s working against you, everything feels harder.

But with the right strategy, it can improve—and open new doors.

Start Taking Control of Your Credit Today

Your credit doesn’t have to control your future. Whether you’re dealing with negative items, low scores, collections, late payments, or confusing credit reports, now is the time to take action. Our credit solutions are designed to help you understand what’s hurting your score, create a clear plan, and start working toward better financial opportunities.

Take the first step today and begin your journey toward stronger credit, more confidence, and a better financial future.

Start Taking Control of Your Credit Today

Your credit doesn’t have to control your future. Whether you’re dealing with negative items, low scores, collections, late payments, or confusing credit reports, now is the time to take action. Our credit solutions are designed to help you understand what’s hurting your score, create a clear plan, and start working toward better financial opportunities.

Take the first step today and begin your journey toward stronger credit, more confidence, and a better financial future.